Current mortgage rates in 2026 are changing rapidly as inflation and Federal Reserve policies impact home loan costs across the US housing market.

Current Mortgage Rates in 2026

mortgage rates in 2026 continue being one of the crucial questions that many home buyers, real estate investors, and current homeowners interested in refinancing have to consider carefully. Interest rates have a direct impact on monthly payments and affordability as well as shape the US housing market situation.

With ongoing fluctuations in inflation, Fed’s actions, and economic uncertainty, many Americans tend to follow mortgage rates when deciding to buy a house or refinance an existing mortgage.

This guide will help you find out more about the recent trends in home mortgage rates, factors influencing their changes, and what is expected to happen soon.

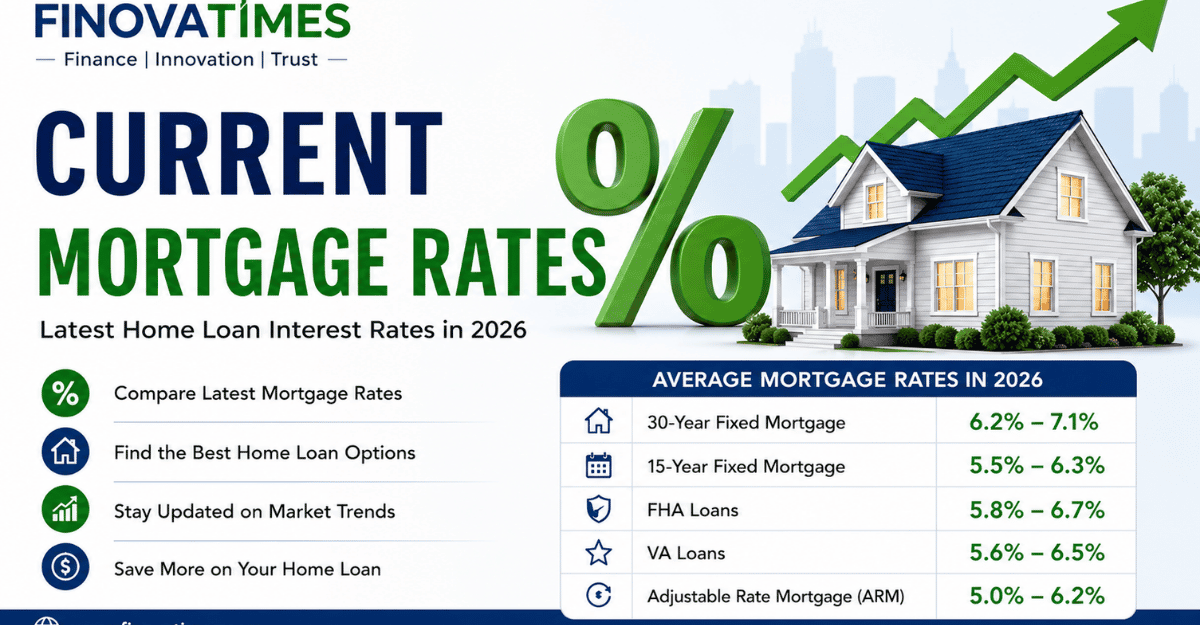

Current mortgage and housing data provided by Reuters.

What Are Current Rates?

Current rates are the rates expressed in interest percentages that lenders charge borrowers for home loans. These rates depend on:

Type of loan

- Credit score of a borrower

- Amount of down payment

- Loan terms

- Economic factors

Mortgage rates can change frequently depending on various economic aspects.

Economic and Federal Reserve news and updates by Bloomberg

Why Current mortgage Rates Are Important

Current mortgage determine how affordable homes can be. Any change in the interest rates has a huge effect on monthly repayments for borrowers.

For instance:

- Lower interest rates can help to save thousands of dollars.

- Higher mortgage rates can affect purchasing power.

- Lower mortgage rates make it more interesting to refinance.

That is why potential buyers should consider current rates very carefully.

Main Factors That Affect Current Rates

Several factors play a critical role in affecting mortgage rates in the U.S.

Federal Reserve

The Federal Reserve influences borrowing costs in many ways. An increase in interest rates results in increased borrowing costs, including mortgage rates.

- Inflation

High inflation levels lead to higher mortgage rates as investors want more profit from their investments.

- Performance of the Bond Market

Mortgage rates are determined by bond yields. Therefore, any changes in bond yields will be reflected in mortgage rates.

- Housing Market Dynamics

Lenders might respond to increased housing demand by changing interest rates.

- Economic State

Borrowing costs tend to increase in case of strong economic growth and decrease during recession.

Statistics for the mortgage industry and lending trends by Bankrate

Are Rates Expected to Decrease in 2026?

According to many housing industry specialists rates can slowly fall if inflation becomes less and the Fed stops raising its interest rates.

However, they could stay unstable due to:

- Economic instability around the globe

- Strength of the labor market

- Energy prices

- Risks in the banking industry

Several forecasters think that rates can approach the 5% level if the economic environment becomes better.

When Is It the Best Time to Purchase a House?

The ideal timing to buy a house does not depend on correctly guessing the market but your financial status.

Specialists advise:

- To enhance your credit rating

- To compare various lenders

- To save money for an additional down payment

- To look for opportunities for refinancing

Even in cases when the mortgage are now relatively high, the price of houses may still grow in competitive markets.

Tips for Getting Better Mortgage Interest Rates

Here are some tips on how to get better loan interest rates:

- Boost Your Credit Score

- Better credit scores earn lower interest rates.

- Make a Larger Down Payment

- More down payment means less lender risk.

Shop Around for Different Lenders

Different lenders might provide better terms and lesser fees.

Opt for Shorter Loan Tenure

Fifteen-year loans typically have lower interest rates compared to thirty-year mortgages.

Pay Off Outstanding Debts

Having less debt will help borrowers secure loan approvals.

Trends in Mortgage Refinancing

Currently, many people are waiting for better opportunities to refinance their homes. With decreasing mortgage interest rates in late 2026, more people will likely be motivated to refinance their mortgages.

Lloyds HSBC NatWest Rule Changes: Introduction of New De-banking Laws

Benefits of Refinancing a Mortgage

By refinancing, borrowers can:

- Have smaller monthly payments

- Shorten loan tenure

- Access their home’s equity

- Consolidate debts

- Housing Market Forecast

The US housing market is expected to stay strong even with the rise in borrowing costs, thanks to the limited availability of homes and the sustained demand for housing in various markets.

According to experts in real estate, there is:

- Modest increase in home prices

- Slow stabilizing in mortgage rates

- Rising need for refinance mortgages

- Strong competition in housing in urban areas

Conclusion

The mortgage rates that currently exist will continue influencing the US housing market in 2026. It is recommended that buyers and homeowners pay close attention to economic developments, policies from the Federal Reserve, and lending rates offered by different lenders before making important decisions.

Even though the rates have been increasing significantly from past years, there are still chances for borrowers to get favorable mortgages for their homes.

Home loan interest rates by Forbes Advisor

Student Loan Forgiveness Changes Hit Middle Class Hard.

Abdul Rehman is the founder and editor of FinovaTimes a digital-first financial media platform covering global markets, artificial intelligence, investing, business, and economic trends.

With a strong focus on modern financial journalism and data-driven storytelling, he specializes in translating complex market developments into clear, accessible insights for a global audience. His editorial work spans AI innovation, Wall Street trends, stock market analysis, macroeconomics, and emerging technologies shaping the future of finance.

Under his leadership, FinovaTimes has developed a modern newsroom approach inspired by leading global financial media brands, combining real-time reporting, high-impact digital publishing, and audience-focused financial content.

His work emphasizes clarity, credibility, and forward-looking analysis across the rapidly evolving global economy.